The latest report from the Intergovernmental Panel for Climate Change (IPCC) released on April 4, 2022 calls for fast action to stabilize the climate, listing a broad range of opportunities enabling compliance with the commitments made in the 2015 Paris agreement.

Each successive assessment report from the IPCC since the first one in 1990 has conveyed ever-increasing alarm. This third installment of the IPCC’s Sixth Assessment Report (AR6) notes the possibility of a 1.5°C scenario receding rapidly but possible with immediate action. Barring such urgent action, by the next Conference of Parties COP27 in Egypt in December, a 1.5°C possibility will be beyond reach.

Per UN chief Antonio Guterres, the report is “a litany of

broken promises… a file of shame cataloguing empty promises”. Going further, he

states “We are on a fast track to climate disaster.… This

is not fiction or exaggeration, it is what science tells us will result from

our current energy policies.”

Among the disaster scenarios: “major

cities under water, unprecedented heat waves, terrifying storms, widespread

water shortages, the extinction of a million species of plants and animals.”

Background – AR6 Working Groups:

This report comes from working group three (WG III) of AR6.

Topics covered in AR6 by respective groups are:

- WG I: The Physical Science Basis – report released in August 2021.

- WG III: Impacts, Adaptation and Vulnerability – February 2022.

- WG III: Mitigation of Climate Change – April 2022.

Focus of AR6 WG III:

The IPCC AR6 WG III report addresses carbon mitigation pathways discussed in earlier IPCC reports and emphasizes two additional pathways: carbon removal and industrial decarbonization.

The report brings demand side mitigation into primary focus. Along with behavioral and lifestyle changes for consumers, advice to planners also, to frame public service in the context of demand rather than supply (methods of fulfilment). Decent Living Standards can be achieved with lower energy expenditure than previously thought.

With the observation that ‘An increasing share of emissions can be attributed to urban areas’, buildings receive special attention in the report, assessed under the SER framework (Sufficiency, Efficiency, Renewable).

The report also emphasizes the need for much greater investment along with technological innovation in climate solutions.

Positive trends:

IPCC notes movement towards goals over the past decade, which has seen:

- A drop of 85% in the cost of solar energy, 55% in wind power;

- electric vehicles market growing a hundred-fold;

- over 20% of Carbon emissions subject to carbon taxes or trading schemes;

- over 50 counties legislated emissions-reducing climate laws;

- 24 countries having reduced emissions consistently;

- climate targets covering emissions rising from 49% to around 90% globally;

- emissions growth rate declining to 1.3% per year, from 2.1% in previous decade.

Challenges:

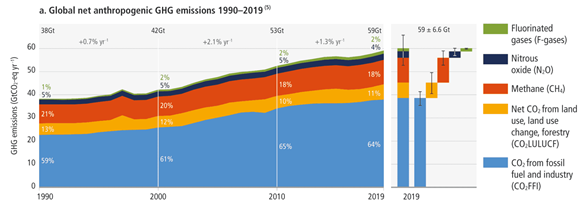

Though the rate of increase declined, in absolute terms the global total for greenhouse gas emissions (GHG) over the last decade increased to an average of a record 56 billion tons per year.

The total carbon budget remaining for the rest of the century, compliant with a 1.5°C goal, is greatly depleted already and will certainly be overshot in the absence of unforeseen technological innovations or socioeconomic/behavioral shifts.

Current Nationally Determined Contributions (NDCs) – country level pledges – are grossly inadequate to meet the 1.5°C goal and minimally supportive of a reasonable shot at 2°C.

There are large investment gaps (project finance) and implementation gaps (rapid deployment).

Retaining a 1.5°C target:

Despite it appearing improbable, the goal of 1.5°C retains urgency because the upper limit of 2°C agreed upon in the Paris accords was reported in a subsequent IPCC report in 2018 to cause unacceptably greater impact. Among ecosystem damage differences between the top and bottom of the range, by 2100:

- Global sea level rise 10 cm lower;

- Arctic Ocean ice-free in summer once per century compared with at least once per decade;

- Coral reef decline of 70-90 percent, opposed to more than 99 percent.

The measures needed to contain the warming at 1.5°C have stringency and a requirement of immediacy rendering its overshoot likely. See below.

Requirements for the 1.5°C target:

The IPCC established for a 1.5°C target an emissions limit of 500 billion additional tons of Carbon Dioxide (CO2, contributing most of the Carbon to the atmosphere) between 2020 and 2100, a period of eight decades. At the current remaining balance of 400 billion tons and current emissions rates, this limit is reached within the decade rather than by the end of the century.

Other requirements include a reduction of fossil fuel usage from 2019 levels, by 2050: Coal 95%, Oil 60%, Gas 45%. Global emissions must peak before 2025 and fall by 43 percent from 2019 levels by 2030.

2°C Scenarios:

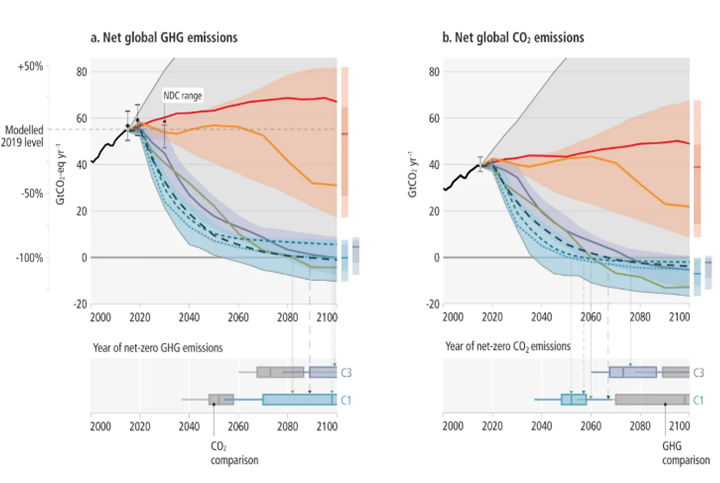

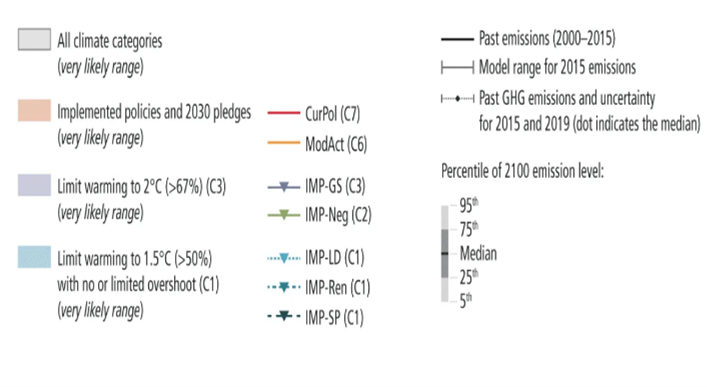

The focus remains on 1.5°C as a target, even with likely overshoot, also because settling upon a 2°C target does not make the challenge significantly less difficult. The pathways towards the higher figure do not diverge as much as might be expected, as indicated through the magenta and cyan bands in the graphic below that was produced by AR6 WGIII.

There is of course a range of possibilities within the hopefully bookended targets of 1.5°C and 2°C tagged by the Paris Agreement, as indicated in the charts and legend above.

Energy Transition:

With national economic engines dependent mostly on fossil fuels, an energy transition (from fossil fuels to green) that supports development and growth imperatives is not yet convincingly feasible financially though efficiencies and cost reductions are demonstrably taking effect.

Between 2010 and 2019, the Energy Intensity of the global economy – energy required for GDP increase – has decreased by 2% per year, an indicator of increasing efficiency in output generation. And for the production of the energy itself, carbon emissions per unit of energy – Carbon Intensity – have decreased, at a rate of 0.3% per year over the same period, indicating a shift towards green energy.

Paris agreement imperatives for Carbon Intensity decrease, however, are rates of 3.5% per year in a 2°C scenario and 7.7% in a 1.5°C scenario.

Fossil Fuels in the Mix:

In any warming scenario within the range stipulated by the Paris Agreement, there may now be no new unabated fossil fuel projects, and existing powerplants and refineries will need to be wound down sooner than the currently determined lifespans that attracted initial investment. Abatement technologies such as Carbon Capture Use and Storage (CCUS, also abbreviated CCS) have not received the required priority and investment over past decades to have been developed to a point of feasibility at present.

The report notes: ‘If investments in coal and other fossil infrastructure continue, energy systems will be locked-in to higher emissions, making it harder to limit warming to 2°C or 1.5°C (high confidence). Many aspects of the energy system – physical infrastructure; institutions, laws, and regulations; and behavior – are resistant to change or take many years to change.’

It further acknowledges: ‘Limiting warming to 2°C or 1.5°C will strand fossil-related assets, including fossil infrastructure and unburned fossil fuel resources (high confidence). The economic impacts of stranded assets could amount to trillions of dollars. Coal assets are most vulnerable over the coming decade; oil and gas assets are more vulnerable toward mid-century. CCS can allow fossil fuels to be used longer, reducing potential stranded assets’.

IPCC modeling does assume in all its scenarios that there will be residual emissions by 2050 that will require abatement either through chemical processes like CCUS, or through ecological methods like reforestation and ecosystem restoration.

Chemical processes are prohibitively expensive currently (for a ton of Carbon, around $600), with no clear indication of their commercial feasibility under present conditions despite hope for exponential advancement. Efficiencies and an accelerating drop in costs of solar energy generation are presented as an example of such advancement, though that has required decades in the making.

Ecological solutions appear low-hanging fruit but pose their own challenges, such as reduction of agricultural land and the need for maintenance of trees, which can themselves become the source of carbon emissions in the case of forest fires in conditions of extreme drought.

Mitigation Options Available:

The report notes with optimism that given the urgent action required, there are options to halve emissions by 2050 in all sectors. It identifies:

- Energy sector transitions – renewable energy, alternative fuels, improved energy efficiency;

- consumer behavior changes – waste-minimization in consumption, public transport;

- smart urban planning – compact cities, transport electrification, zero-carbon buildings;

- circular economy, waste-minimization, efficient low-to-zero-carbon processes in production;

- smart agriculture, forestry and land use.

The need to integrate urban mitigation and adaptation strategies for cities to address climate change is pressed urgently, with reference to the double threat of rising emissions and more frequent extreme weather events.

Demand side mitigation is emphasized: it can result in emissions reductions of 40-70% compared with that from pledges made by governments prior to 2020. For planners, it offers a paradigm: ‘People demand services and not primary energy and physical resources per se. Focusing on demand for services and the different social and political roles people play broadens the climate solution space.’

Investment Requirements:

Financial flows towards climate change mitigation need to be scaled up 3 to 6 times the current levels by 2030 for even a 2°C scenario. These may target clean energy, efficiency, transport, agriculture and forestation as outlined in the mitigation options listed above.

There is adequate Global capital and liquidity to meet requirements but closing the investment gap will require stronger alignment of public sector finance and policy and clear signaling of support and commitment by governments and international organizations.

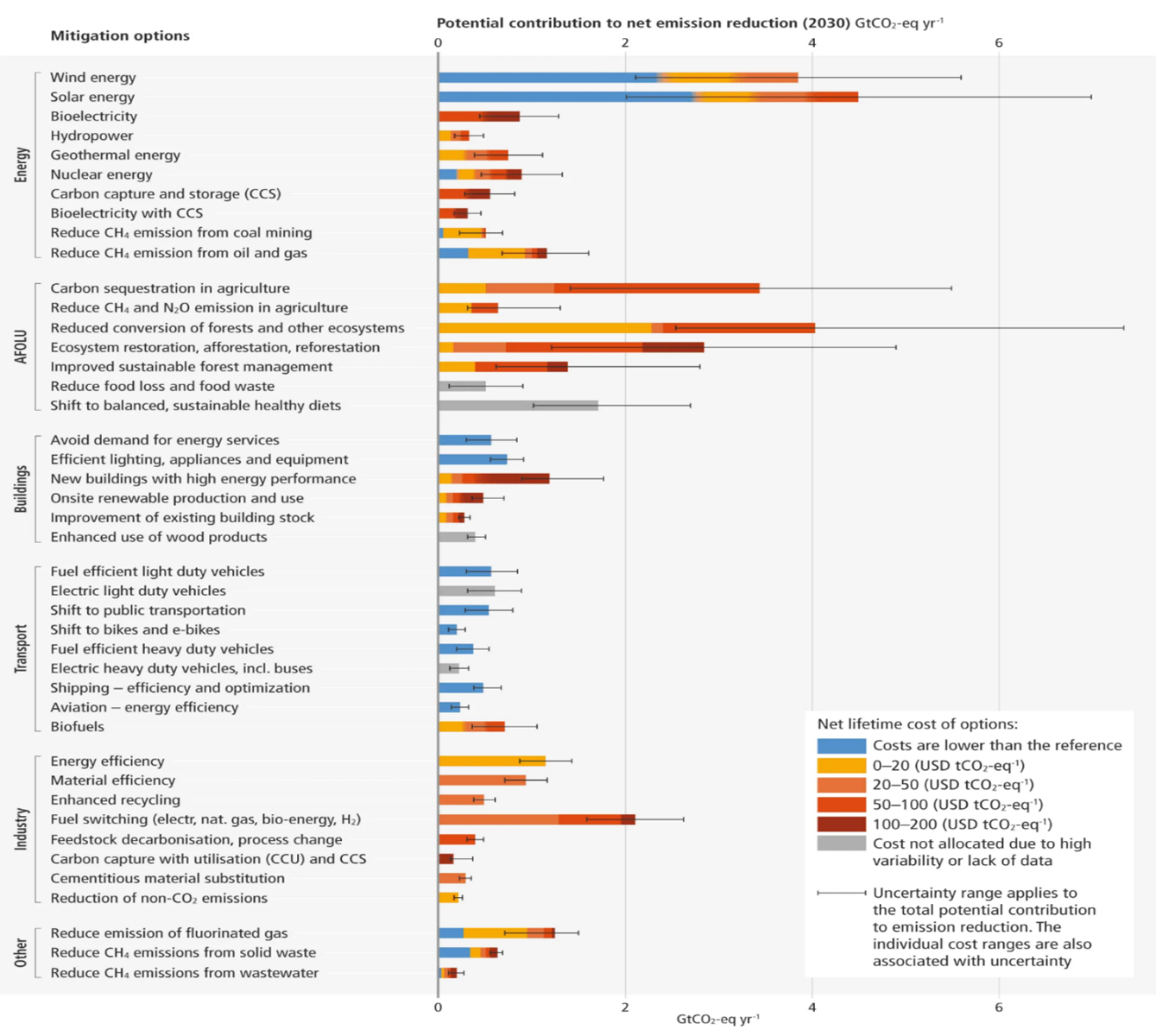

The graphic from the report listed below provides in color-coded form the costs of various mitigation options and their impact to net emissions reduction by 2030, scaling up in gigatons. Blue is below current reference cost. Mustard signifies less than $20 per ton. Increasing costs are indicated in darker color bands per the legend at the bottom right of the table.

Key Takeaways:

Raising yet higher the already alarming warnings from earlier reports, this report appears to present the last now or never opportunity before a 1.5°C possibility is gone forever.

It proposes immediate action with much greater financial flows and demand side management, summarized below:

- Reduction in fossil fuel use, development of abatement technology for residual emissions;

- Carbon removal projects, chemical and ecological;

- Socio-cultural and behavioral change, supportive policy;

- Clean energy investment.

© Haseeb Ahmed, The Stanwork Group